No doubt, chain hotels and independent properties should and do co-exist – to the benefit of guests. But how do corporate chains truly differ and why are they expanding so rapidly all over the world. MKG Hospitality’s Michael Komodromou looks at trends and initiatives with chain hotels.

Before we look at some of the key trends and initiatives with corporate chain hotels, we should first clarify the main benefits of such products. For instance, are they really a better option – either from a guest or investor perspective?

Like in other sectors, chain products have their pros and cons. And of course it should really be judged on an individual basis. Sure, many independent hotels have their uniqueness and charm, and might very well be better than the chain hotel down the road – or perhaps simply offer guests a different experience to the ‘expected’.

However, the simple reality is that in this modern day, fast paced and interconnected world, chain or independent, all hotels need to be plugged in and have as big of a network as possible.

{kind=link}

Even those that are not part of a chain (franchised or managed), are either affiliated to a consortium such as Small Luxury Hotels of the World (SLH) or must at very least be connected to an online travel agent (OTA), such as Bookings.com, Expedia, and Lastminute.com.

Ultimately, it comes down to a chain being more complete in offering three crucial criteria:

- Marketing/Branding

- Standards (in product and service), and

- Distribution channels (i.e. via OTA, GDS, central reservation system, loyalty programmes, corporate contracts, agreements with DMCs and tour operators such as TUI, etc.)

Beyond this, each hotel chain also greatly differs from each other. These days, there are so many types of chain brands – small, medium to large international groups – that essentially there is a great variety of styles, products, and positioning.

At the end of the day, you could say that the bigger the chain, the more supporting options and exposure. The top five groups in the world, Intercontinental Hotels Group (IHG), Hilton, Marriott, Wyndham, and Accor surely offer more options in brand portfolio, global marketing, and distributional channels.

However, their standards might not be for everyone. Other chains might offer more and more specialised niche and are much better suited for the type of product, location or clientele, such as Four Season, Jumeirah, Six Senses, Shangri-La, Steigenberger.

Global trends with corporate hotel chains

Considering the above, it is understandable that we have seen a massive increase in chain hotel developments over the last decade and more, as groups continue to penetrate new markets, and with new sophisticated brands and products.

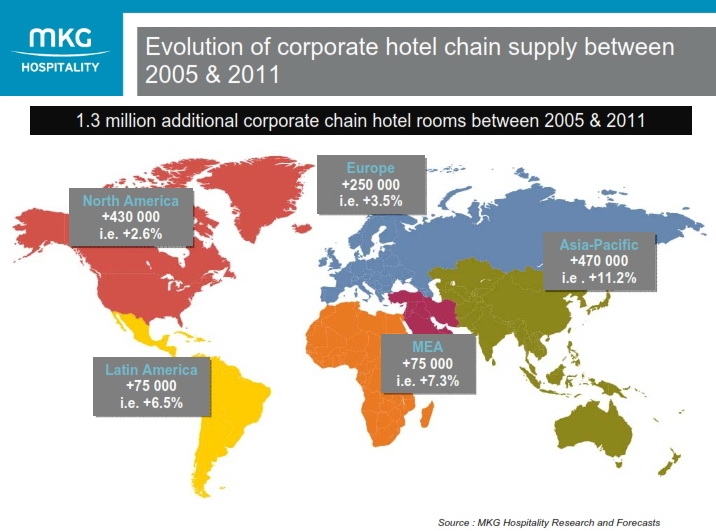

Between 2005 and 2011, there was an injection of 1.3 million chain hotel room around the world. Most growth came in the Asia-Pacific region, with an increase of 11.2%, followed by the Middle East & Africa at 7.3% and then Latin America 6.5%. Europe’s chain supply increased by 3.5% and the North America 2.6%.

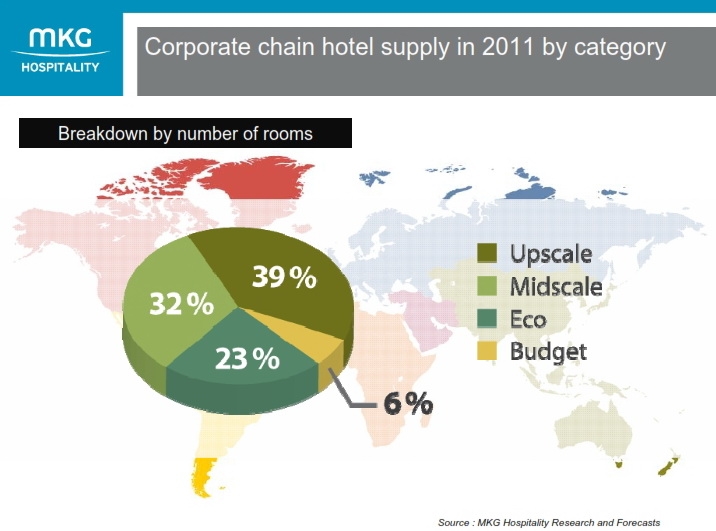

Globally, most developments came in the upscale segment, with almost half a million rooms and an increase of 4%, followed by economy chain products with over 400,000 rooms and an increase of just over 6%.

In emerging destinations, upscale products certainly tends to be the norm. This is very much the case in places such as the Middle East & Africa region for instance, where currently almost 75% of total chain supply is in the upscale and luxury segment.

Then in order for a market to be considered mature, it must develop economy and budget supply. We mainly see this happening in North America and Europe, both with a much more even balance between the categories. No doubt their tourism industries are also far more advanced, thereby facilitating consistent demand for all types of chain products.

{kind=link}

The best synergy can be drawn to the aviation industry’s low cost airline model. This encouraged a different type of traveller, such as lower-paying (business or leisure) and city breaks. In turn, this drove demand for lower priced accommodation.

Following the global financial crisis in 2009, chain supply in the world continued to increase considerably, as many projects were still being completed. Pipeline developments, however, were either cancelled or postponed. In 2010, chain supply remained stable and then in 2011 decreased significantly.

At present, there are around 18 million hotel rooms around the world, of which, 6.7 million are corporate chains. North America has by far the largest chain penetration rate, with 67% of its total supply being chain hotels. Indeed, this is where chain groups first took off. As such, most of the world’s leading brands are also US based, such as the likes of Hilton, Marriott International, Wyndham, Choice, Carlson Rezidor Hotel Group, Starwood Hotels & Resorts, to name but a few.

The largest hotel supply overall (chain and independent) is found in Europe, however only 26% are corporate chains. Some of the main European based players being Accor (also the largest group in Europe), IHG, Group du Louvre, NH Hoteles, Sol Melia, TUI and Whitbread.

In Asia-Pacific, corporate chains have 28% share, in Latin America 20% and in the Middle East & Africa 23%.

Looking at these chain penetration rates, it is understandable why these regions are where most chains are focusing their development strategies, as North America is saturated. Asia is fast emerging economically, the Middle East has great potential for chains, and Africa is still in its infancy. All these markets also heavily revolve around new-build projects. Europe is a mature market yet still with fairly low penetration rates. However, new chain supply is a mixture of new-build and independent properties converting.

Because of these new market developments, we are also seeing the emergence of new hotel groups from other parts of the world, such as Home Inns, Jin Jiang and 7 Days Group from China, JAL, Prince Hotels and APA Hotels from Japan, Banyan Tree, Anatara Hotels and Six Senses from Southeast Asia, Mantra Hotels and Toga Group in Australia, Taj Hotels and Indian Hotels Company in India, and Rotana in the Middle East. No doubt this trend will continue.

{kind=link}

Another interesting trend worth noting is the correlation between chain penetration rate and a market’s economic development. Countries with higher GDP per capita tend to have much higher chain penetration rates, such as in the GCC, the US and Scandinavian countries.

Types of chain hotels; management contracts & franchised

Over 70% the world’s chain supply is in the upscale and midscale segments. Of course usually these are much larger properties, naturally requiring greater support and access to more selling channels.

These properties also tend to have a management contract structure as opposed to being franchised. Over 46% of upscale chain hotels and approximately 72% of upper upscale properties in the world are managed by chains. Whereas lower categories are easier to maintain and have much less operational elements, i.e. staff, facilities, product specifications. As such, these segments tend to be dominated by franchise agreements: over 63% of chain midscale hotels in the world are franchised, 75% in the economy category and 47% in budget.

In more mature markets such as North America and Europe, international hotel brands have an established presence and considered to be mainstream assets. Chains are also a lot more confident in franchising their products in these markets, justified by more advance economies and tourism environments, better developed transport and accessibility, as well as more experienced operators and investor-owners. No doubt, these mature markets are a model for hotel development and growth.

Other markets around the world are less developed. These regions are typical of emerging and less mature markets, where chain supply is dominated by management contracts, allowing chains to maintain a certain level of assurance.

{kind=link}

Most are also in the upscale segment, which is almost always the first to be developed when establishing a new destination. However in some cases, investor-owners in emerging markets prefer to manage their own products, independently or if possible, via a franchise. This is particularly true in extremely underdeveloped or unfamiliar markets where international chains have poor local presence and where operations can be very market specific, therefore also more complex.

Finally, it is worth touching on new types of chain hotels. As markets develop and mature, demand also increases for specialised or niche products. Perhaps none more obvious then the aparthotel concept, with the likes of IHG’s Staybridge Suites and Accor’s Adagio emerging on to the scene, among many other brands; likewise, the same group’s boutique concepts Indigo and MGallery.

Cultural aspects have also been heavily worked into new concepts, such as Rotana’s Rayhaan brand, respecting the beliefs and culture of Islam. Meanwhile, other groups focus one core aspect, such as MGM Resorts International with casinos and entertainment or Walt Disney Attractions.

Of course many brands simply find their niche by targeting either business guests (*Millennium & Copthorne Hotels, Hyatt, Scandic, Carlson Rezidor) or leisure (TUI), top-level luxury (Fairmont Raffles Hotels, Mandarin Oriental, Aman Resorts), or hard budget (Hotelformule1, Premiere Classe, Travelodge).

*Although hotels target both business and leisure guests depending on their exact location, these groups have been highlighted due to their tendency to develop properties in strong business destinations.

By Michael Komodromou (Market Development & Research Manager, MKG Hospitality, mkg-hospitality.com )

MKG Hospitality publishes annual regional hotel reports, looking at the macro environment, total hotel supply, corporate chain supply, leading groups, pipeline growth, and key performance trends. This year marks the first Middle East & North Africa Report (2013 edition). For more information or to obtain a copy of these reports, contact m.komo ‘at’ mkg-hospitality.com