Leading tourism and hotel consultants, MKG Hospitality looks into the growing popularity of economy and budget hotel products – supply and demand.

Economy and budget hotel products will no doubt be the next major boom in the hospitality industry. In fact, we’re already seeing all the signs, particularly when observing mature markets, such as Western Europe and North America – generally considered as providing the best indication of how a global trend will transpire.

Corporate chain economy segments (1-, 2- and 3-stars) are fast becoming the number one choice for both business and leisure travellers, as they are deemed to offer optimal value-for-money. The new wave of these hotels are especially offering a product and service considered to be better quality (i.e. in terms of facilities and service), but at a much more affordable price. A similar situation to what happened with low cost airline carriers, such as EasyJet.

These products contribute to a destination’s overall goal of attracting an increasing number of arrivals. They diversify a destination’s available product and provide more options for visitors – not everyone wants to or can stay in upscale hotels these days – therefore a greater market share can be captured. Indeed, a destination should not be mono-segment, but rather have an even-spread of hotel products. This balance opens up the market and fuels more visitors.

More importantly for owners and investors, economy and budget hotels are more resilient towards a bubble burst. They endure external threats much better, such as economic recessions, low consumer purchasing power, a declining currency, pressure from competing markets and other global uncertainties, whilst offering owners a more secure Return on Investment (ROI), due to much lower operational expenses.

In the industry, the main hotel performance indicators to be observed include:

Occupancy Rate (OR) – a percentage indicating the number of room nights sold (compared to number available) – it is how we often measure demand.

Average Daily Rate (ADR) – measurement of hotel's pricing scale, derived by dividing actual daily revenue by the total number of sold rooms.

Revenue per Available Room (RevPAR) – Measuring commercial performance, and representing the success a hotel is having at earning revenue from its room inventory (multiplying ADR by OR).

Hotel Supply Trends

Between 1999 and 2009, the world’s budget and economy supply recorded moderate average annual growth at 3.4% (2% for the mid- and upscale segments). Most of this growth occurred in Europe and North America, with 134,000 and 246,000 newly created rooms, respectively.

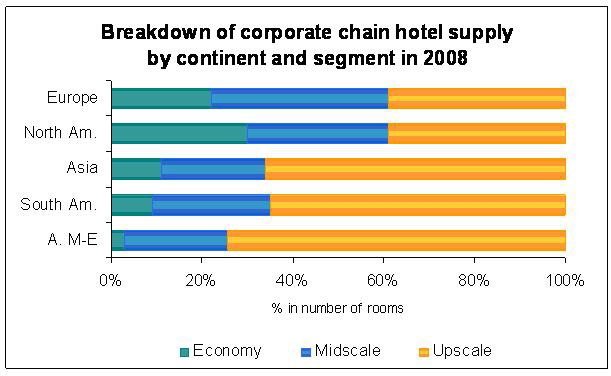

North America remains the most balanced market in the world in terms of category breakdown, followed closely by Europe. Meanwhile, other regions are still considered to be relatively non-mature.

Although the European budget and economy hotel supply remains less developed (20% of total supply) compared to the US, it is growing year-on-year, boosted by the continued penetration into non-mature markets, such as Central and Eastern Europe. This is also a good sign for hotel groups and investors, indicating that there is still ample room for expansion.

{kind=link}

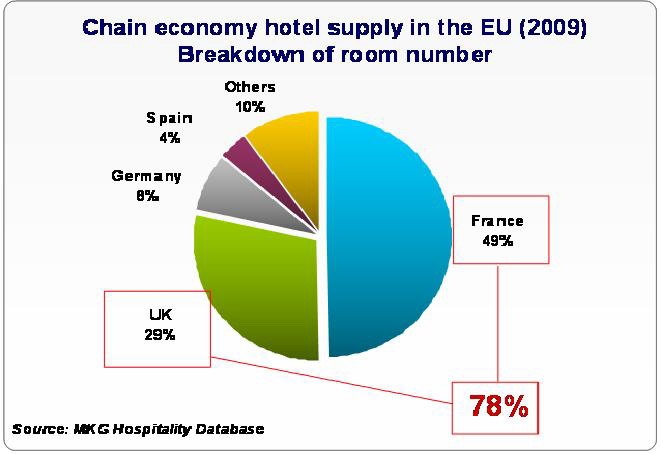

France and the UK were the pioneering European markets. In fact, together they still currently account for 78% of Europe’s economy hotel supply.

France proved to be the first major influential market, with its key players, Accor’s Ibis, Etap Hotel and HotelF1 (former Formule 1), as well as B&B and Louvre Hotel’s Première Classe and Campanile. Following this popularity, UK brands such as Premier Inn, Travelodge and Holiday Inn Express were established and to this day, enjoy significant growth – between 1999 and 2009 the UK’s economy hotel supply increased by an average of 9.1%.

Other major European markets, such as Germany and Spain have also started to see their economy hotel supply increase (now with 8% and 4% of the EU’s share), primarily fuelled by French and local chains (i.e. Motel One in Germany).

{kind=link}

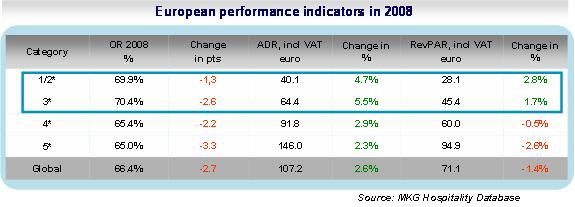

Hotel Performance Indicators in 2008

In terms of performance, budget and economy hotels prove to be the most resilient in Europe over this recent challenging period.

In 2008, they were the only segments with a positive RevPAR growth – 2.8% increase in the budget category and 1.7% in economy. Although they both experienced a reduction in occupancy, a healthy ADR is what allowed them to achieve these results.

By comparison, the midscale segment recorded a 0.5% decrease in RevPAR, whilst the upscale category was the most affected, with a 2.6% drop.

Clearly, travellers have become a lot more price conscious in recent months, especially the business sector, cutting back on expenses in order to battle the financial downturn.

We can expect to see this continue well into 2009, and hopefully start to recover in 2010, when the economy rebounds and average hotel prices are at their lowest, thus encouraging purchasing.

{kind=link}

Popular Brands

For the past three years, the economy hotel industry’s metamorphosis has been making headlines all over Europe. Their new positioning has become a widespread phenomenon, with the introduction of new innovative concepts and re-branding of existing products, such as hotelF1 and the new generation Campanile or B&B Hotels. This new status of quality value-for-money is now no longer an option, but rather a prerequisite.

Technical innovations, modern construction techniques and design, as well as more efficient operational methods are what have allowed the budget and economy segments to transform and prosper. This is why there is a critical network size and critical size per hotel in this segment, in order to make operations feasible.

Accor’s Ibis brand is by far the largest economy brand in Europe, with currently almost 70,000 rooms under this flag. This is a slight increase of 3% from 2008. The most dynamic growth came from Travelodge, with a 13.1% increase, Whitbread’s Premier Inn with 12.4%, and IHG’s Express by Holiday Inn. In terms of hotel groups, the two French groups Accor and Louvre Hotels still dominate the European market, closely rivaled by IHG.

{kind=link}